Enterprise SSD Demand Surges Amid AI Server Expansion

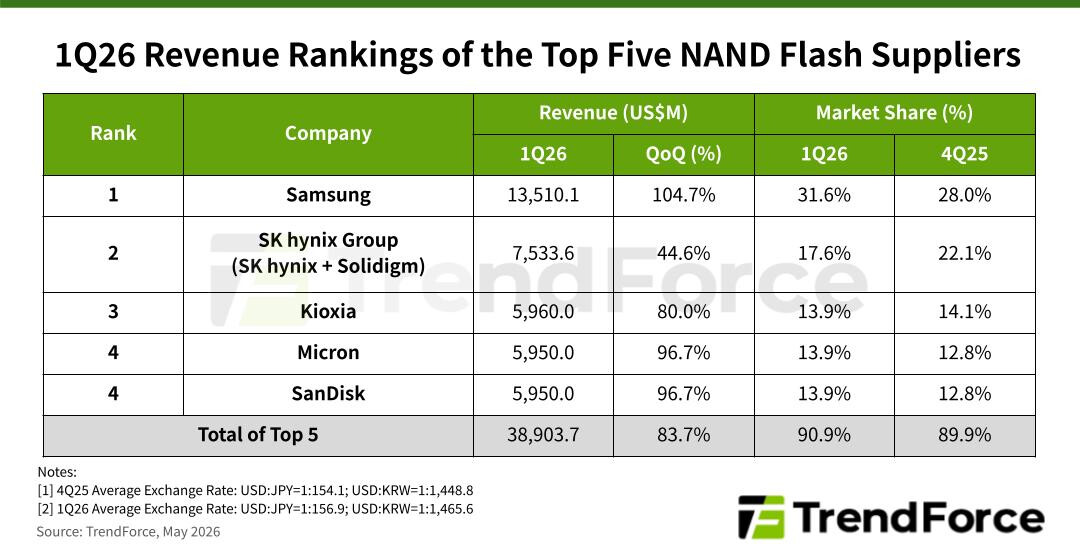

According to the latest research from TrendForce, the global NAND Flash market experienced unprecedented growth in the first quarter of 2026. Cloud service providers (CSPs) worldwide accelerated their investments in enterprise SSDs, driven by the need for high-speed data transfer and vast storage capacities to support expanding AI server infrastructure. At the same time, a persistent shortage of traditional HDDs prompted many storage-related orders to shift toward QLC enterprise SSDs. This combination of soaring demand and limited supply led to average selling prices (ASPs) for NAND Flash products exceeding industry expectations. As a result, the combined revenue of the top five NAND Flash suppliers surged by 83.7% quarter-over-quarter (QoQ), surpassing US$38.9 billion.

Market Outlook for 2Q26: Supply Constraints and Strong Server Demand

Looking ahead to the second quarter of 2026, the imbalance between supply and demand is expected to persist. While higher memory costs and increased end-product prices have softened demand in the smartphone and PC segments, robust server orders are anticipated to offset these declines. Most NAND Flash suppliers project continued shipment growth through the second quarter, with pricing strategies likely to maintain elevated ASPs.

Performance of Leading NAND Flash Suppliers in 1Q26

Samsung maintained its leadership position in the NAND Flash market, leveraging favorable contract pricing and a significant increase in server-related bit shipments. The company reported US$13.51 billion in NAND Flash revenue for 1Q26, representing a remarkable 104.7% QoQ increase—the highest among the top five suppliers. Samsung’s market share expanded from 28% to 31.6% during this period.

SK hynix Group, which includes SK hynix and its subsidiary Solidigm, secured second place with approximately US$7.53 billion in revenue, marking a 44.6% QoQ increase and a 17.6% market share. The group’s growth was driven by rising ASPs and a steady stream of orders for high-capacity QLC enterprise SSDs, particularly benefiting Solidigm.

Kioxia delivered a strong performance as well, with revenue climbing 80% QoQ to US$5.96 billion and maintaining its third-place ranking with a 13.9% market share. The company benefited from the overall surge in NAND Flash prices and favorable market conditions, achieving notable gains in both revenue and profitability.

Micron also saw significant gains, with its NAND Flash revenue rising 96.7% QoQ to US$5.95 billion. This growth allowed Micron’s market share to rebound to 13.9%, tying with Sandisk for fourth place.

Sandisk recorded a dramatic increase in its data center business, with QoQ revenue growth exceeding 200%. The company’s strategic shift toward high-value product offerings paid off, as its overall 1Q26 NAND Flash revenue matched Micron’s at US$5.95 billion, reflecting a 96.7% QoQ increase and a 13.9% market share.

Industry Trends: Limited Capacity Expansion and Focus on High-Capacity SSDs

TrendForce forecasts that major NAND Flash suppliers will add virtually no new production capacity in 2026. With AI-driven demand expected to remain strong, supply shortages are likely to persist throughout the year. By the end of 2026, NAND Flash products featuring 200 layers or more are set to become the industry standard. Production resources will continue to be heavily allocated to server storage applications, further accelerating the adoption of high-capacity QLC enterprise SSDs across the market.